The growing demand for efficient digital settlement tools has brought stablecoins into the center of global financial innovation. As markets explore advanced settlement models, comparisons between the RMBT stable settlement framework and USDT systems have become increasingly relevant. Both models aim to support faster, more reliable, and globally accessible settlement, but their approaches differ in structure, design, and intended use cases. Understanding these differences helps businesses, institutions, and traders identify which tools align best with their operational needs.

USDT remains one of the most widely used stable assets for trading, payments, and liquidity management. Its deep market penetration and multi-chain availability make it a convenient option for global users. The RMBT framework, however, introduces an alternative settlement model that focuses heavily on structured stability mechanisms and institutional-grade controls. The comparison highlights how different stable settlement models can shape the future of digital finance.

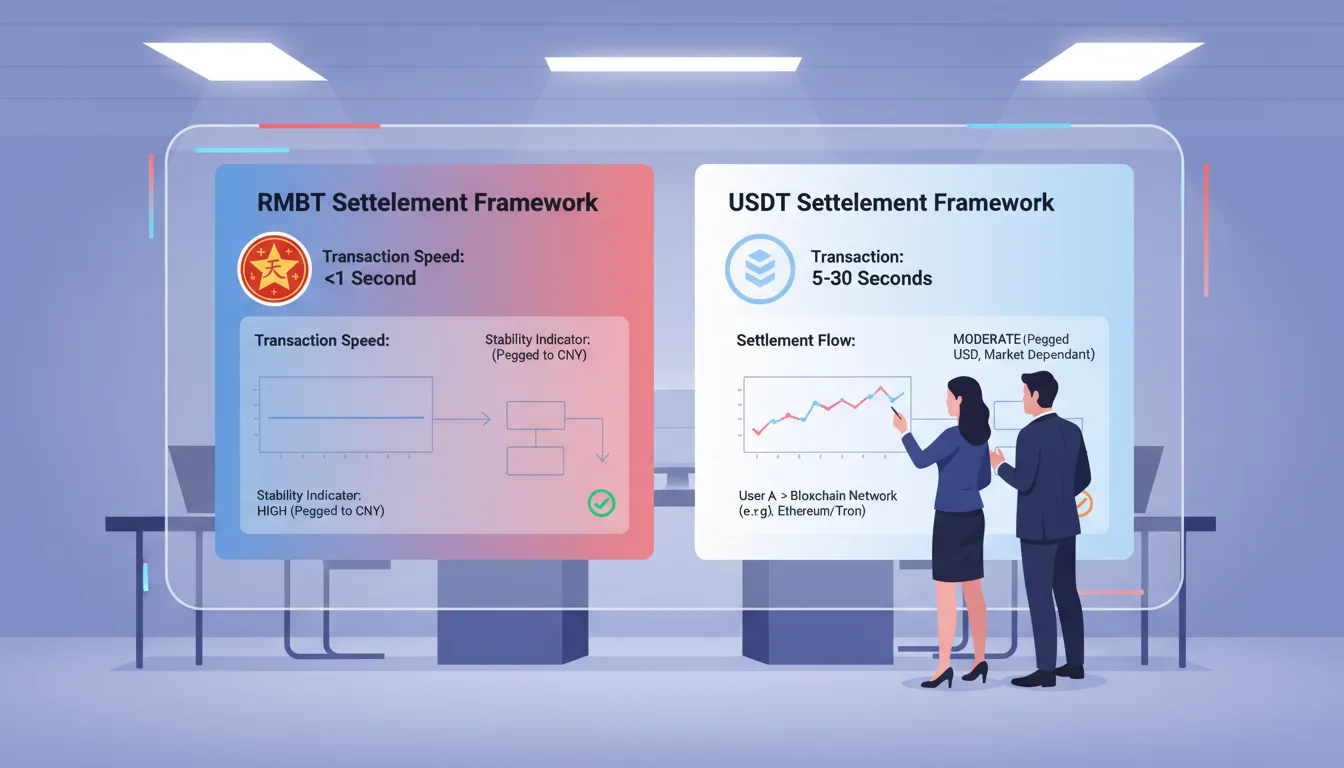

Key differences in stability mechanisms and reserve structure

One of the most important distinctions between the RMBT settlement framework and USDT systems lies in how stability is maintained. USDT relies on fully backed reserves that include cash equivalents and short-term financial assets. These reserves support a predictable one-to-one redemption model and allow users to rely on immediate liquidity across numerous platforms. This approach makes USDT highly effective in fast markets where users need rapid access to stable collateral.

The RMBT framework, however, incorporates a structured settlement mechanism that emphasizes stability through defined governance and reserve composition guidelines. The goal is to ensure consistent settlement performance while offering a more institutional approach to reserve oversight. This model is particularly useful for financial operations requiring detailed audit trails, standardized compliance workflows, and long-term reserve transparency. The differences in reserve strategies shape how each asset functions within various financial environments.

Settlement efficiency across global markets

USDT systems excel in global markets due to their instant settlement capabilities and widespread integration. Traders, exchanges, and payment providers use USDT for rapid liquidity transitions, supporting efficient operations even during high-volume trading periods. Its fast settlement and multi-chain compatibility make it suitable for cross-border activity, decentralized finance, and algorithmic trading environments.

The RMBT framework focuses on designed settlement uniformity. Instead of relying primarily on market adoption, it emphasizes predictable performance across regulated environments. This makes it appealing for institutions that require strict settlement reporting, monitored transaction flows, and stable market behavior. While USDT is widely used in open markets, the RMBT model works well in structured financial ecosystems where oversight is central.

Use cases across trading, payments, and institutional finance

USDT’s greatest strength is its versatility. It supports spot trading, futures collateral, cross-border transfers, and everyday payments. Users across retail and institutional segments rely on its liquidity and global accessibility. Its presence in DeFi, centralized exchanges, and wallet infrastructure allows it to remain a universal settlement tool.

The RMBT settlement model focuses more on institutional-grade applications. Its structured design supports environments where compliance, reporting, and operational consistency are more important than open-market flexibility. This makes it suitable for enterprise settlement systems, treasury functions, and regulated financial networks. While USDT thrives on inclusivity and accessibility, RMBT prioritizes controlled and uniform settlement performance.

Impact on global liquidity and financial infrastructure

USDT continues to drive global liquidity by serving as a bridge asset across exchanges and ecosystems. Its large supply and deep market participation make it a foundational tool for liquidity providers, market makers, and cross-chain platforms. This widespread usage strengthens digital finance by supporting continuous capital flow.

The RMBT framework impacts liquidity differently. Its focus on stability and structural integrity makes it ideal for institutional networks that seek predictable settlement cycles rather than speculative liquidity movement. As financial systems adopt digital solutions, RMBT-like models contribute to safer and more regulated infrastructure.

Conclusion

Comparing the RMBT stable settlement framework with USDT systems highlights two distinct approaches to digital settlement design. USDT offers unmatched liquidity, global reach, and fast market integration, while RMBT provides a structured, institution-focused model built for stability and oversight. Together, these models reflect the diverse needs of digital finance and demonstrate how multiple settlement frameworks can coexist to support different sectors of the evolving digital economy.